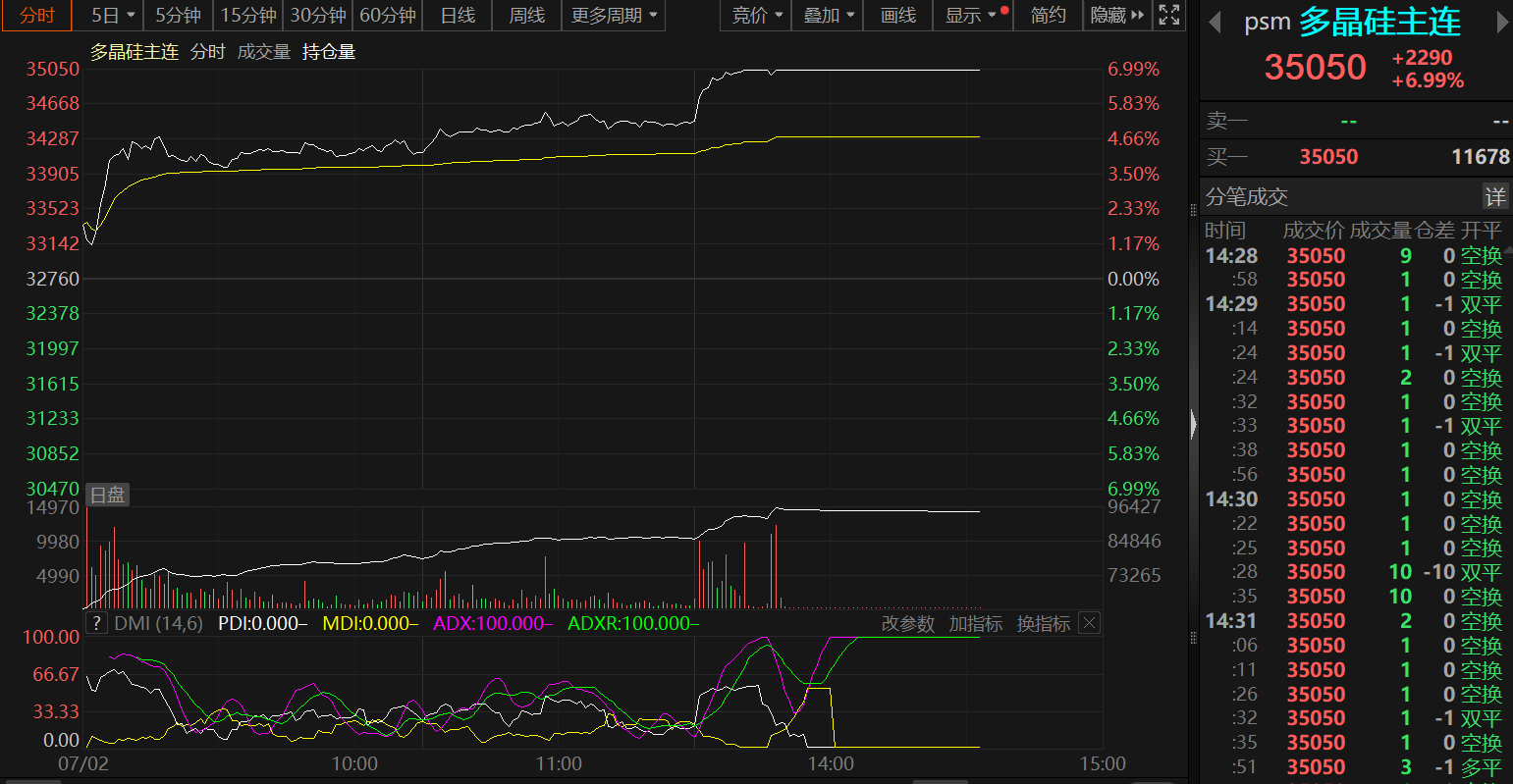

SMM July 2 news: After opening in the early morning of July 2, the most-traded polysilicon futures contract surged rapidly, directly spiking and hitting the limit-up board around 13:48 in the afternoon. It eventually locked in the limit-up with a 6.99% gain, closing at 35,050 yuan/mt, marking its first limit-up since futures listing.

Regarding the reasons for this sharp rally in polysilicon futures prices, SMM attributes it primarily to the following factors:

On the news front, according to Xinhua News Agency, Xi Jinping, General Secretary of the CPC Central Committee, President of the State, and Chairman of the Central Military Commission, presided over the sixth meeting of the Central Financial and Economic Affairs Commission on the morning of July 1. The meeting emphasized advancing the construction of a unified national market in depth, focusing on key challenges, regulating enterprises' low-price disorderly competition according to laws and regulations, guiding enterprises to improve product quality, and promoting orderly exit of outdated capacity.

Meanwhile, in the market, SMM survey shows that top-tier enterprises have voluntarily unified cost-based price hikes. According to SMM spot quotes, today's N-type polysilicon price index rose by 2 yuan/kg to 36 yuan/kg, with a single-day gain as high as 5.88%.However, SMM learned that under current quotes, downstream transactions were nearly absent, with the overall market in a wait-and-see mode.

》Click to view SMM PV product spot quotes

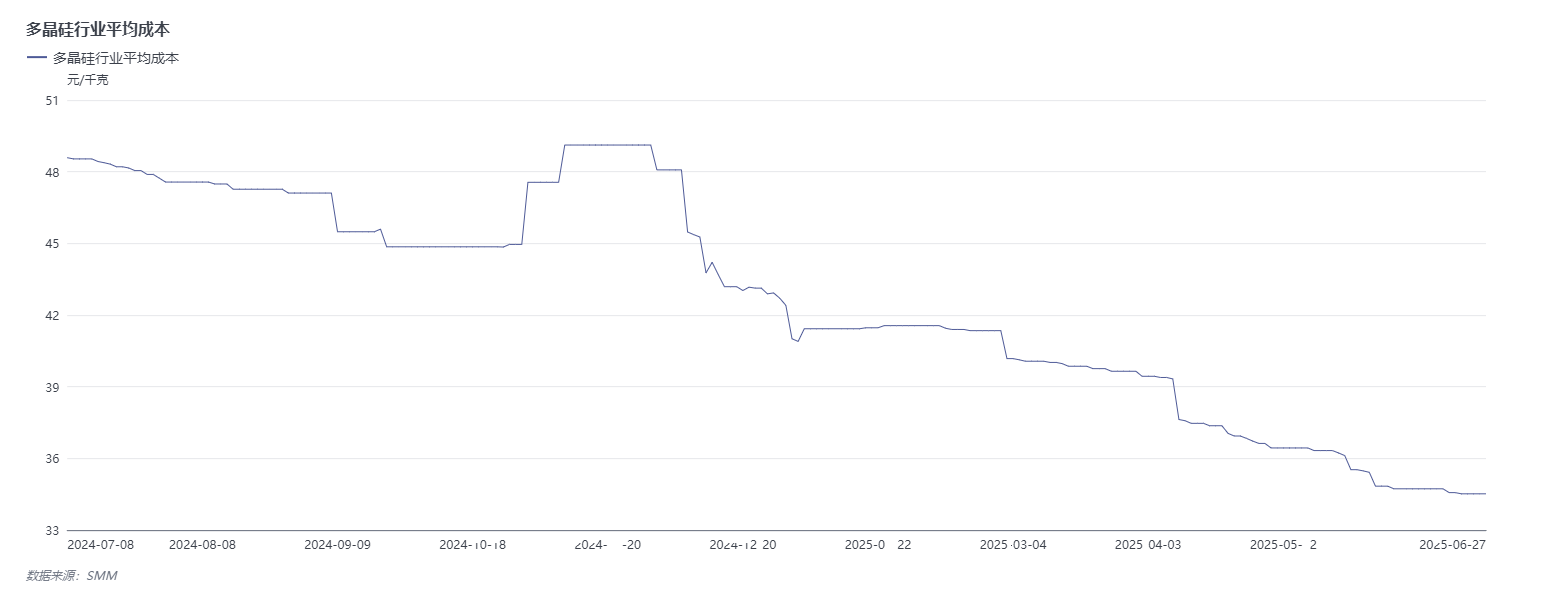

SMM data shows that as of June 27, the average industry cost of polysilicon dropped to 34.52 yuan/kg. The recent decline of the N-type polysilicon price index to 34 yuan/kg had already approached the industry's average cost line.

Overall, however, polysilicon fundamentals lack substantial positive support. Regarding the closely watched July production schedule, SMM survey indicates the final June schedule showed no significant changes from earlier expectations. In July, several top-tier enterprises increased production while some second- and third-tier players implemented production cuts or shutdowns, resulting in an overall production increase of approximately 5,000-6,000 mt MoM.

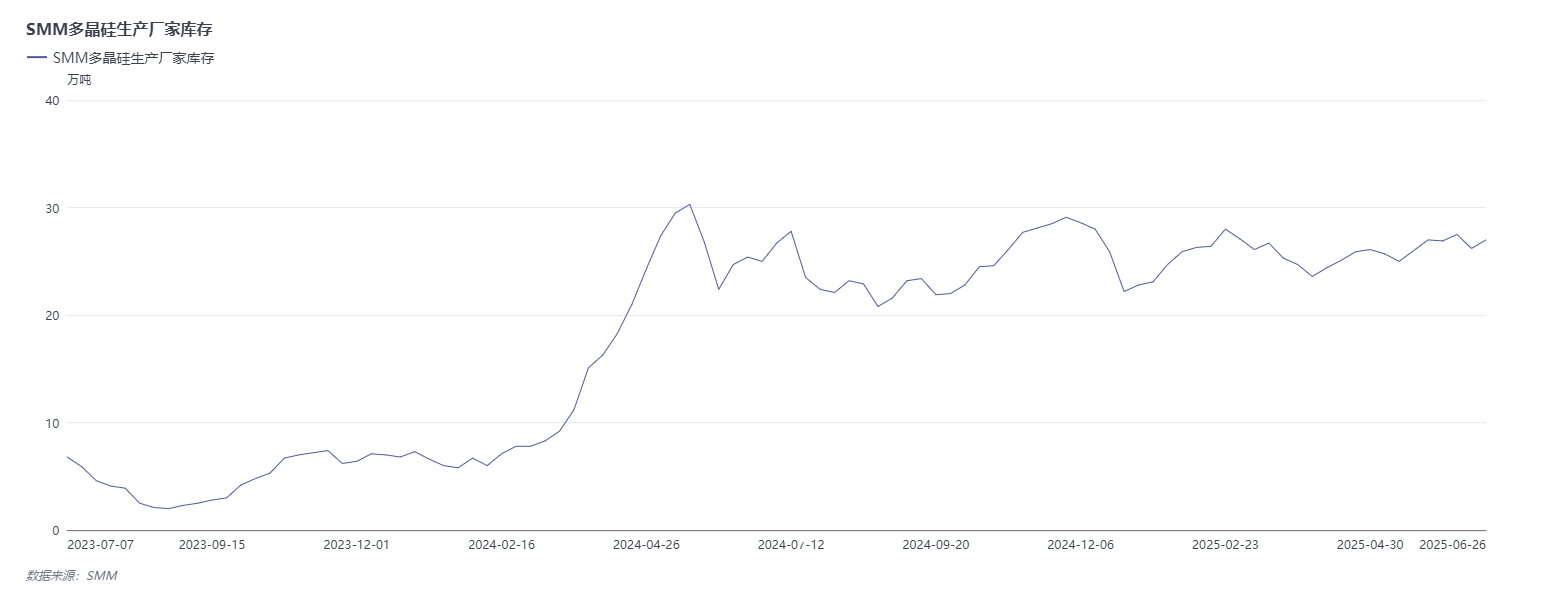

Inventory-wise, SMM understands polysilicon inventory still faces considerable pressure with significant disparities among enterprises. Overall inventory rose recently due to reduced order signing. As of June 26, SMM polysilicon producer inventory totaled 270,000 mt, remaining at a multi-year high for the same period.

Notably, as one of China's most cut-throat competition industries, PV has long been regarded as the "main force" in rectifying such practices. On February 25, 2025, the State Administration for Market Regulation held a fair competition symposium inviting enterprises from PV, e-commerce, and automotive sectors to discuss measures against cut-throat competition. The June 29 People's Daily article "Achieving High-Quality Development by Eliminating Cut-Throat Competition" also published significant commentary on PV anti-competition themes, stating that behind PV's cut-throat competition lies temporary supply-demand mismatch impacts. Increased external uncertainty, insufficient domestic demand, and oversupply contradictions have intensified industry competition, exacerbating cut-throat competition to some extent. Additionally, it was mentioned that the key to breaking free from "cut-throat competition" lies in balancing the roles of a proactive government and an efficient market.

In response to the national call to "combat cut-throat competition," the PV industry has been taking its own measures. One such example is the China Photovoltaic Industry Association (CPIA) guiding enterprises to sign a voluntary production control and self-discipline agreement. On June 30th, the planned 30% production cuts by most domestic glass enterprises in July also represent a significant move by the PV glass industry to avoid "cut-throat competition" and prevent a vicious cycle in the market caused by intensified competition among enterprises.

According to the SMM survey, some glass enterprises have recently begun planning their subsequent production schedules. Regarding domestic PV glass production in July, SMM believes that despite the increase in production days, the expansion of production cuts may lead to the first decline in glass production since the Chinese New Year this year. It is estimated that glass supply in July will decrease to around 45GW.

Moreover, there is also positive news from overseas. On July 1st local time, the US Senate passed the "Big and Beautiful" bill, strongly advocated by Trump, which removed the excise tax on wind and solar projects at the last minute. Spurred by this news, solar stocks on the US stock market surged on Tuesday.

It is reported that the excise tax on wind and solar projects, originally mentioned in the bill, was seen as a way to help the US reduce its dependence on China's clean energy supply chain. However, considering that many local solar and wind farms still rely to a certain extent on foreign parts and the supply chain dominated by China, the implementation of this tax may increase the costs of local solar and wind farms. Research institution Rhodium Group predicts that this will lead to a 10% to 20% increase in the construction costs of wind and solar energy. The American Clean Power Association (ACP) also estimates that the new excise tax will add $4 billion to $7 billion in costs for US clean energy companies over the next decade.

Therefore, the removal of the excise tax on wind and solar projects at the last minute is a significant positive for local wind and solar stocks.

Affected by the continuous rise in domestic polysilicon futures, the index of the PV equipment sector also surged by over 3% during the trading session. In terms of individual stocks, more than six stocks, including Shuangliang Eco-Energy, Yijing Optoelectronics, OJing Technology, Cybrid Technologies, and Tongwei Co., Ltd., hit the daily price limit during the trading session.

China Securities' research report states that in the short term, due to weakening demand and the expectation of some production resumptions in the polysilicon sector, polysilicon prices are still in the process of hitting bottom. However, with current prices already approaching the cash costs of top-tier enterprises, it is expected that the downside room for further price declines is limited. Additionally, from the policy perspective, the PV industry, as one of the key industries in China's efforts to address cut-throat competition, has a relatively clear direction for the future supply side, and is expected to reverse the current state of losses across the entire PV industry chain.

![[SMM PV News] Armenia Hits 1.1 GW Solar Capacity,](https://imgqn.smm.cn/usercenter/qQwIB20251217171741.jpg)

![Spot Market and Domestic Inventory Brief Review (February 5, 2026) [SMM Silver Market Weekly Review]](https://imgqn.smm.cn/usercenter/tSwaX20251217171735.jpg)